The Benefit Emergency Fund brings to your personal finance strategy cannot be overstated—it’s like a safety net that protects you from life’s unexpected challenges. An emergency fund is a stash of money set aside to cover sudden expenses, such as medical bills, car repairs, or job loss, without derailing your budget or plunging you into debt. This article explores why an emergency fund is essential, how it supports your financial goals, its key benefits, and practical steps to build one, ensuring you’re prepared for whatever life throws your way.

What is an Emergency Fund?

An emergency fund is a dedicated savings account for unexpected, urgent expenses. Unlike savings for planned goals like a vacation or a new phone, this fund is for true emergencies—situations that threaten your financial stability or basic needs. Financial experts recommend saving 3–6 months’ worth of living expenses, though even $1,000 can be a strong start. The fund acts as a buffer, helping you avoid high-interest debt or dipping into retirement savings when crises arise.

Key Benefits of an Emergency Fund

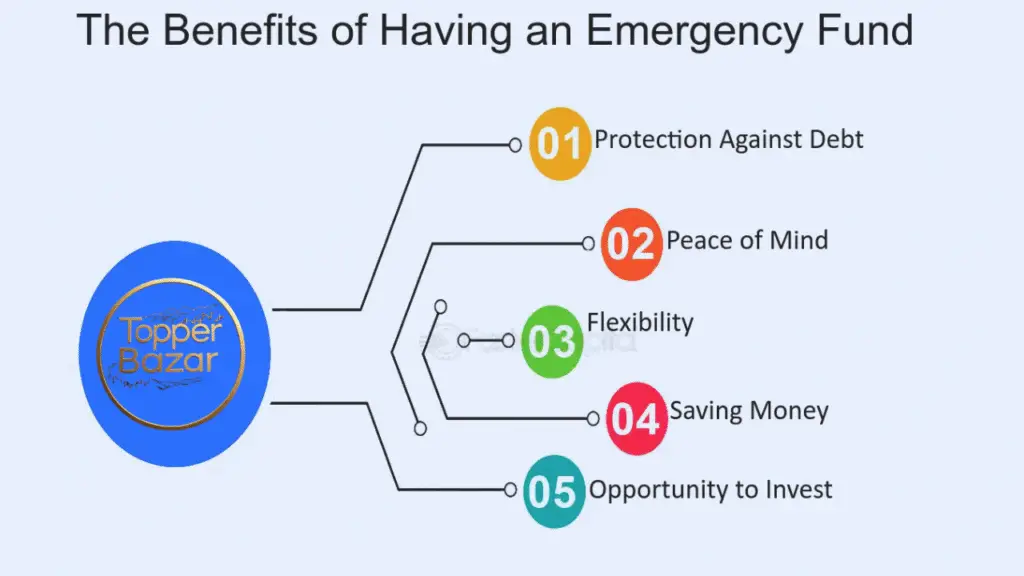

1. Protection Against Debt

One major benefit of an emergency fund is avoiding debt during unexpected events. For example, if a $2,000 medical bill arises and you don’t have savings, you might put it on a credit card with 18% interest. Paying only the minimum could take years and add hundreds in interest. With an emergency fund, you cover the bill outright, saving money and stress.

2. Financial Stability During Job Loss

Losing a job can disrupt your income, making it hard to pay for essentials like rent or groceries. An emergency fund covering 3–6 months of expenses gives you time to find new work without panic. For instance, if your monthly expenses are $2,000, a $6,000 fund provides a 3-month buffer, allowing you to focus on job hunting rather than financial survival.

3. Peace of Mind

The emotional benefit of an emergency fund is huge. Knowing you have money set aside for emergencies reduces anxiety about “what if” scenarios. This peace of mind lets you focus on other goals, like investing for retirement or saving for a home, without worrying about sudden setbacks.

4. Preserves Your Investments

An emergency fund prevents you from withdrawing money from long-term investments, like retirement accounts or stocks. Early withdrawals from accounts like a 401(k) or IRA often come with penalties and taxes, plus you lose future growth from compound interest. For example, withdrawing $5,000 from a retirement account at age 40 could cost you $20,000+ in future gains, assuming a 7% annual return. An emergency fund keeps these investments intact.

5. Supports Budgeting and Financial Goals

An emergency fund complements your budget by acting as a safety valve. If an unexpected cost arises, you won’t need to cut back on essentials or stop saving for other goals. This stability helps you stick to your financial plan, whether it’s paying off debt or investing in a mutual fund.

How Much Should You Save in an Emergency Fund?

The ideal size depends on your situation, but here are general guidelines:

- Starter Fund: Save $1,000 as a beginner’s emergency fund. This covers small emergencies, like car repairs or minor medical bills.

- Standard Fund: Aim for 3–6 months of living expenses, typically $6,000–$18,000 for most households. This is ideal for stable single-income households.

- Larger Fund: Save 6–12 months if you’re self-employed, have irregular income, or support dependents, as your financial risks are higher.

How to Build an Emergency Fund

Building an emergency fund takes time, but small, consistent steps add up. Here’s how to start:

- Set a Goal: Decide on an initial target, like $1,000, and a long-term goal, like 3 months’ expenses. Clear goals keep you motivated.

- Automate Savings: Set up automatic transfers to your emergency fund after payday. Even $25 per paycheck builds momentum.

- Redirect Windfalls: Put bonuses, tax refunds, or gift money into your fund to boost it quickly.

- Replenish After Use: If you use your fund for an emergency, prioritize rebuilding it to maintain your safety net.

Where to Keep Your Emergency Fund

Choose an account that’s accessible but earns interest:

- High-Yield Savings Accounts: Offer 3–5% interest, far better than traditional savings accounts (0.01–0.5%). Online banks like Ally or Marcus often have the best rates.

- Money Market Accounts: Similar to high-yield savings but may offer check-writing or debit card access for emergencies.

- Avoid Risky Investments: Don’t put your emergency fund in stocks or bonds, as their value can drop when you need cash. Keep it liquid and safe.

Tips to Maximize the Benefit of an Emergency Fund

- Review Regularly: Check your fund every 6–12 months to ensure it matches your current expenses, especially after life changes like a new job or baby.

- Combine with Saving Challenges: Use the 52-week challenge (saving $1,378 yearly) or no-spend challenge to jumpstart your fund. A saving challenges calculator can estimate totals.

- Stay Disciplined: Only use the fund for true emergencies, like medical bills or job loss, not wants like a new gadget.

- Pair with Insurance: An emergency fund works best alongside health, auto, or renters’ insurance to cover larger costs.

Common Mistakes to Avoid

- Not Starting: Waiting for “extra” money delays your fund. Start with $5 weekly if that’s all you can afford.

- Mixing Accounts: Keeping your fund in your checking account risks spending it. Use a separate savings account.

- Underfunding: A $500 fund may not cover major emergencies. Aim for at least $1,000, then build to 3–6 months.

Conclusion

The Benefit Emergency Fund offers is invaluable for anyone serious about personal finance and investing. It protects against debt, provides stability during job loss, preserves investments, and brings peace of mind. By starting small, automating savings, and using a high-yield account, you can build a fund that safeguards your financial future. Whether you’re saving $1,000 or 6 months’ expenses, an emergency fund ensures you’re ready for life’s surprises while staying on track for your financial goals.