Credit Karma is a free credit monitoring service that empowers UK users to track their credit score, access their credit report, and make smarter financial decisions, aligning with personal finance and investing goals in the 2025 UK property market. With house prices expected to rise 2–4% and a buyer’s market offering 12% more homes, Credit Karma helps you build a strong credit profile to secure mortgages or loans. This article explores how Credit Karma works, its benefits and limitations, and how to use it Topper Bazar to support financial goals like homeownership.

What is Credit Karma?

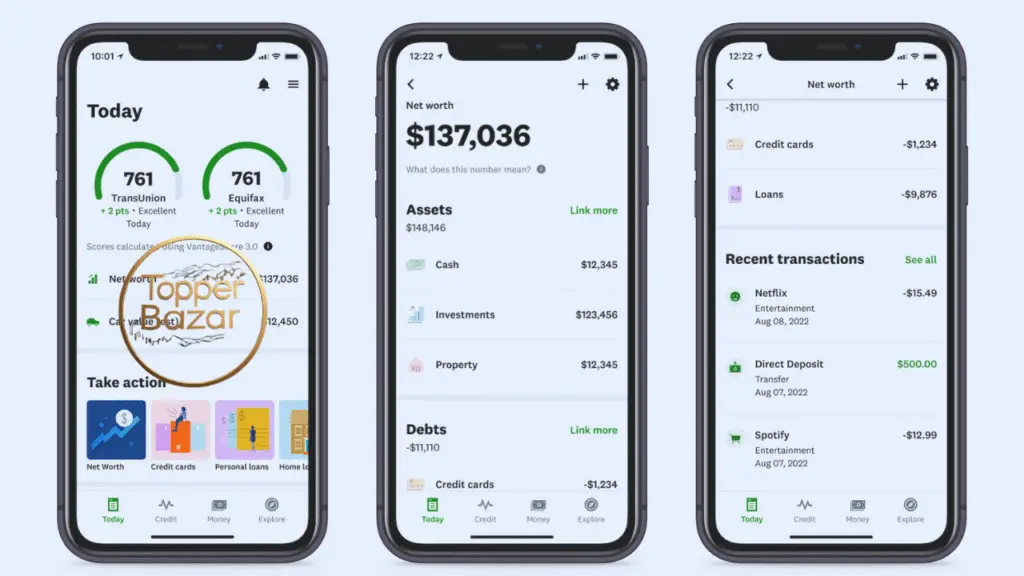

Credit Karma is a UK credit reference agency and broker that provides free access to your TransUnion credit score (0–710) and credit report, updated weekly. Launched in the UK after its U.S. success, it’s owned by Intuit and partners with TransUnion, one of the UK’s three main credit reference agencies (CRAs) alongside Experian and Equifax. By signing up via the Credit Karma website or app, you get insights into your credit history, personalized loan and credit card offers, and tips to improve your score, all without a subscription fee.

How Credit Karma Works

To use Credit Karma, you:

- Sign Up: Create an account with your email, name, date of birth, and address. Verify your identity with questions about your credit history.

- Access Your Score: View your TransUnion credit score (0–710) and report, updated every 7 days, showing payment history, credit utilisation, and account details.

- Get Insights: Receive alerts for credit file changes (e.g., new accounts) and tips on improving your score (e.g., lowering credit card balances).

- Explore Offers: Browse personalized loan and credit card offers based on your score, with Approval Odds to gauge acceptance chances.

Credit Karma labels scores as: 0–565 (Needs Work), 566–603 (Fair), 604–627 (Good), and 628–710 (Excellent). A higher score improves your chances for low-rate loans or mortgages. It’s free, earning revenue as a broker by recommending financial products, with no impact on your credit score from soft searches.

Benefits of Credit Karma

- Free Access: No fees for credit score, report, or alerts, unlike Experian’s £14.99/month CreditExpert service.

- Credit Building: Monitor your score weekly to improve it for mortgages (e.g., 95% LTV loans needing 620+ scores) in 2025’s property market.

- Personalized Offers: View loan and card offers with Approval Odds, helping you choose products you’re likely to get without hard searches.

- Fraud Protection: Alerts notify you of credit file changes, reducing identity theft risks.

- Educational Tools: Tips on factors like payment history (35% of score) or credit utilisation (30%) help you boost your score.

- User-Friendly: The app is easy to navigate, with 11,098 Trustpilot reviews praising its clarity and deal-sourcing features.

Using Credit Karma in the 2025 UK Property Market

In 2025, with a buyer’s market and 2–4% price growth, Credit Karma supports property goals:

- Mortgage Eligibility: A score above 604 (Good) improves chances for 95% LTV mortgages (e.g., £12,500 deposit on £250,000). Monitor weekly to hit 620+.

- Deposit Savings: Use Credit Karma to track credit while saving £150/month in a Lifetime ISA (LISA), yielding £12,600 with a 25% bonus in 7 years for a deposit.

- Loan Planning: Compare low-APR loans (e.g., 5.9% from Santander) for renovations to boost home value by 5–10% (£12,500–£25,000 on £250,000).

- Negotiation Power: A strong score supports mortgage approvals, letting you negotiate 5–10% below asking in a market with 22% of homes unsold after six months.

Steps to Use Credit Karma Effectively

- Sign Up: Visit creditkarma.co.uk or download the app. Provide personal details and verify identity.

- Check Score Weekly: Log in to view your TransUnion score (0–710) and report for updates on accounts or inquiries.

- Follow Tips: Reduce credit card balances below 30% and pay on time to boost your score (e.g., from 566 to 604 in months).

- Review Offers Carefully: Use Approval Odds to select loans or cards, but verify terms (e.g., 6.99% APR, no fees) before applying.

- Monitor Alerts: Enable notifications for credit file changes to catch errors or fraud early.

- Combine with Other Tools: Use ClearScore (Equifax) or Experian’s free score to cross-check, as lenders may use different CRAs.

Tips for Success in 2025

- Boost Your Score: Pay bills on time, keep credit utilisation below 30%, and avoid hard inquiries (e.g., limit loan applications).

- Save with a LISA: Automate £150/month into a LISA for a home deposit, using Credit Karma to ensure a strong credit profile.

- Act Before April: Buy homes before stamp duty thresholds drop (£425,000 to £300,000 for first-time buyers), saving £2,500 on a £350,000 home.

- Target Growth Areas: Focus on Manchester (5% growth) or Northern Ireland (9.5–15.2%) for property investments, using Credit Karma to secure financing.

- Stay Informed: Follow MoneySavingExpert or The Property Podcast for credit and property tips, complementing Credit Karma’s insights.

Credit Karma and Personal Finance

Credit Karma aligns with personal finance by fostering credit health, a cornerstone of wealth-building. A strong score (628+) unlocks low-rate loans or mortgages, supporting homeownership, which builds equity unlike renting. Using Credit Karma to monitor credit while saving in a LISA or high-interest account ensures disciplined investing. For example, a £10,000 loan at 6% APR for renovations, paired with a £12,600 LISA deposit, positions you for a £250,000 home purchase in 2025.

Conclusion

Credit Karma is a free, user-friendly tool for UK residents in 2025, offering weekly TransUnion credit score updates, personalized offers, and tips to build credit. In a property market with 2–4% growth, it helps secure mortgages or loans for homeownership or renovations. Use it to monitor your score, follow improvement tips, and pair with a LISA to save for deposits. By leveraging Credit Karma responsibly, you can strengthen your financial future and achieve long-term wealth in the UK.